I’m Govinda Finn, and this is your Gateway to Japan. In this series, I will share insights into the forces shaping the Japanese economy, while gaining inside access to the key topics driving investment decisions.

Our first focus is corporate governance reform, a cornerstone of Japan’s economic evolution. With the third wave of reforms landing in June 2026, corporate dynamics are changing, reshaping how companies operate, how capital is allocated, and how value is created. So what does that actually mean for portfolios?

In this inaugural article, we spoke with Mr. Uesako, a Japanese equity analyst at Sumitomo Mitsui Trust Asset Management, to get the inside view on progress so far and the outlook ahead.

Corporate governance reform in Japan has shifted from a traditional system—characterised by cross-shareholdings and main bank oversight—towards a market-oriented model aligned with global capital standards. Since the introduction of the Stewardship Code (2014), the Corporate Governance Code (2015), and the Tokyo Stock Exchange’s 2023 PBR initiative, corporate focus has increasingly turned to ROE and share price performance. While early reforms emphasised formal governance changes such as appointing outside directors and conducting share buybacks, attention is now moving to substantive issues, including portfolio restructuring and growth investment. However, progress remains uneven, creating a widening gap between leading and lagging firms and leaving significant revaluation potential in the Japanese equity market.

In the first of a new Gateway to Japan series, Govinda Finn PhD, a Visiting Professor at Tokyo Metropolitan University, finds compelling evidence that asset managers have played a critical role in driving change through sustained engagement with companies. To better understand how Japanese firms have evolved and to explore where they are headed, he interviews senior investment professionals at Sumitomo Mitsui Trust Asset Management, one of Japan’s leading asset managers.

In this first instalment, we present an exclusive interview with Kazuya Uesako, who leads company research and engagement efforts on the front lines.

Govinda Finn Ph.D.

He is a Visiting Professor at Tokyo Metropolitan University and serves as an adviser to Sumitomo Mitsui Trust Asset Management. Previously, he worked at Aberdeen Investments as an economist covering Japan and Developed Asia. He is also a member of the International Advisory Board of the Asia-Scotland Institute.

He holds a Ph.D. from the Graduate School of Economics at Kobe University and was a fellow of the Japan Science and Technology Agency (JST) ‘Next-Generation Pioneering Research Programme’. He also holds a Master’s degree from the School of Oriental and African Studies (SOAS), University of London, and a Bachelor’s degree from the University of Leeds. During his undergraduate studies, he spent one year at the Darla Moore School of Business, University of South Carolina. He also holds the Investment Management Professional qualification.

Volume 1 Interview with Kazuya Uesako – Corporate Research Analyst

Moving beyond ’Compliance’ to an era in which ‘Management Substance Is Put to the Test’

Kazuya Uesako

After joining Sumitomo Mitsui Trust Asset Management, he began his career as an analyst in April 2009. To date, he has covered small- and mid-cap stocks in the automotive components and machinery sectors, as well as the chemicals and financial sectors. Prior to becoming an analyst, he worked in retail sales, corporate pension sales, as a corporate pension consultant, and as a domestic equity passive fund manager.

He graduated from the Department of Applied Biological Chemistry, Faculty of Agriculture, at the University of Tokyo. Sponsored by Sumitomo Mitsui Trust Asset Management, he subsequently completed an MBA at the Graduate School of Business and Finance at Waseda University, receiving an award for outstanding academic performance. He holds the Certified Member Analyst (CMA) qualification awarded by the Securities Analysts Association of Japan and is a licensed Real Estate Transaction Agent.

1. Why did governance reform in Japanese companies begin?

— First, what were the characteristics of the traditional corporate governance model in Japan?

From the post-war period through to the era of high economic growth, Japanese companies developed within a bank-centred financial system. At that time, there was strong demand for capital from companies, and a governance structure known as the ‘Main Bank model’ functioned effectively, whereby banks supplied funds whilst closely monitoring firms.

Within this framework, cross-shareholdings between banks and business partners also became widespread. As these stable shareholders generally supported company proposals, there was little pressure from shareholders for companies to deliver strong performance. Furthermore, corporate management tended to prioritise the stable growth of the company, its employees, and its business partners, rather than the maximisation of shareholder value. As a result, awareness of capital efficiency metrics such as ROE and PBR remained low.

Naturally, this system had its merits at the time. It was, in many respects, a rational model during periods when companies had a substantial need for capital, such as the high-growth era.

— Why did the traditional governance model reach its limits, and why did Japan move towards reform?

The background to this shift lies in significant changes in the Japanese economy and corporate structure. While the Main Bank model was well suited to the high-growth period, this framework persisted long after Japanese companies had matured and large corporations had accumulated sufficient capital. Ideally, there should have been a transition from bank-centred governance to management more focused on capital markets, but this shift did not progress sufficiently.

This situation was compounded by the 2008 global financial crisis (the Lehman Shock) and the 2011 Great East Japan Earthquake. Amid a growing sense of economic stagnation, the Abe administration, which took office in 2012, made economic revitalisation its top priority. As part of this agenda, a growth strategy - the so-called ‘third arrow’ of Abenomics - was introduced to complement monetary and fiscal policies, with corporate governance reform positioned as a key pillar.

In short, there was a clear need to improve the profitability and capital efficiency of Japanese companies, as well as to enhance the overall growth potential of the Japanese economy. Driven by this sense of urgency, alongside underlying structural changes, corporate governance reform in Japan began in earnest.

—What do you think has been the most significant factor in transforming Japanese companies through corporate governance reform to date?

In my view, the most significant factors have been changes in shareholder composition and policy direction from the government.

Prior to the reforms, relationships with banks and internal corporate logic often took precedence over stock market considerations, and management did not necessarily pay close attention to share prices or ROE. However, as cross-shareholdings were gradually unwound and the influence of both domestic and international investors increased, companies shifted fundraising and engagement priorities to capital markets.

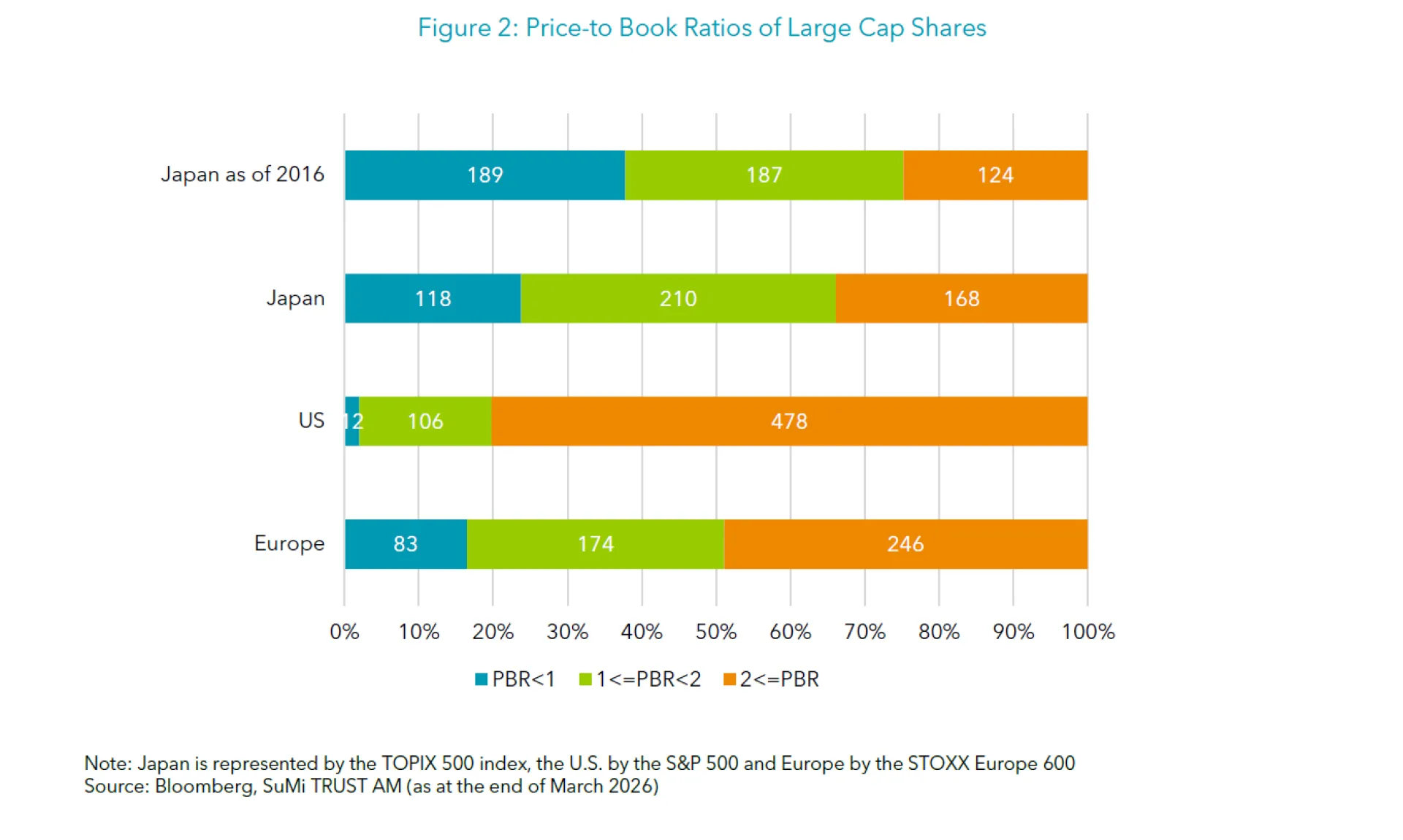

Even companies that may not respond solely to shareholder pressure have been influenced by a prevailing sentiment that ‘we have no choice but to change because the government is calling for it’. With the introduction of clear benchmarks—such as the Stewardship Code in 2014, the Corporate Governance Code in 2015, and the 2014 Ito Report, which established 8% ROE as a desirable target, alongside calls from the Tokyo Stock Exchange (TSE) to improve PBR—corporate behaviour began to shift more decisively.

In particular, the TSE’s 2023 request for companies with low PBR to improve their ratios had a profound impact. The message - namely, that companies must pay close attention to share prices and capital efficiency -was unambiguous, further heightening corporate awareness of these metrics.

There were initially concerns in Japan as to whether a principles-based, ‘soft law’ approach would be effective. However, the establishment of clear benchmarks, such as the 8% ROE target and the TSE’s focus on companies with PBR below 1x, created tangible pressure. In essence, corporate governance reform in Japan has moved beyond a phase of formal compliance and entered a stage in which companies are being tested on their ability to deliver genuine improvements in corporate value.

2. How have the reforms changed corporate behaviour?

— Are there any actual examples where the effects of the reforms are becoming apparent?

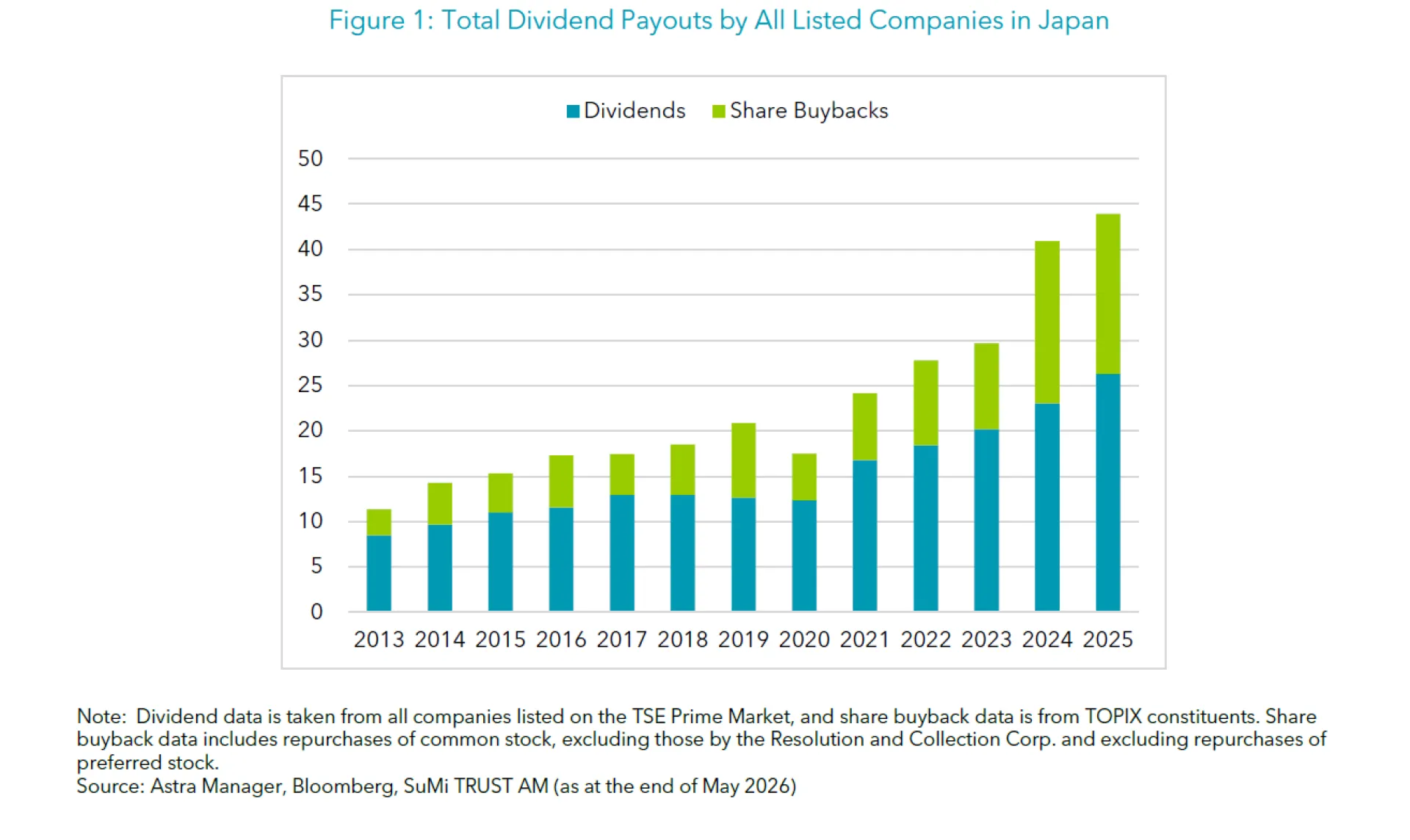

In the banking sector, for example, attitudes towards PBR and ROE have changed markedly. While banks are benefiting from improved earnings driven by the Bank of Japan’s normalisation of monetary policy, they are also accelerating the disposal of cross-shareholdings in order to deploy capital more effectively.

The sale of such holdings reduces the corporate governance discount and tends to have a relatively direct positive impact on PBR. However, PBR and ROE do not necessarily move in tandem or to the same extent. The disposal of cross-shareholdings does not, in itself, structurally enhance ROE; what matters fundamentally is how the proceeds are subsequently utilised.

By allocating proceeds from disposals to shareholder returns and growth investment, capital efficiency improves, leading to a rise in ROE. Furthermore, under Japanese GAAP (JGAAP), gains on the sale of strategic shareholdings are recognised in the income statement. While this provides a temporary boost to ROE, it is a one-off effect and should be distinguished from sustainable improvements in underlying earnings power.

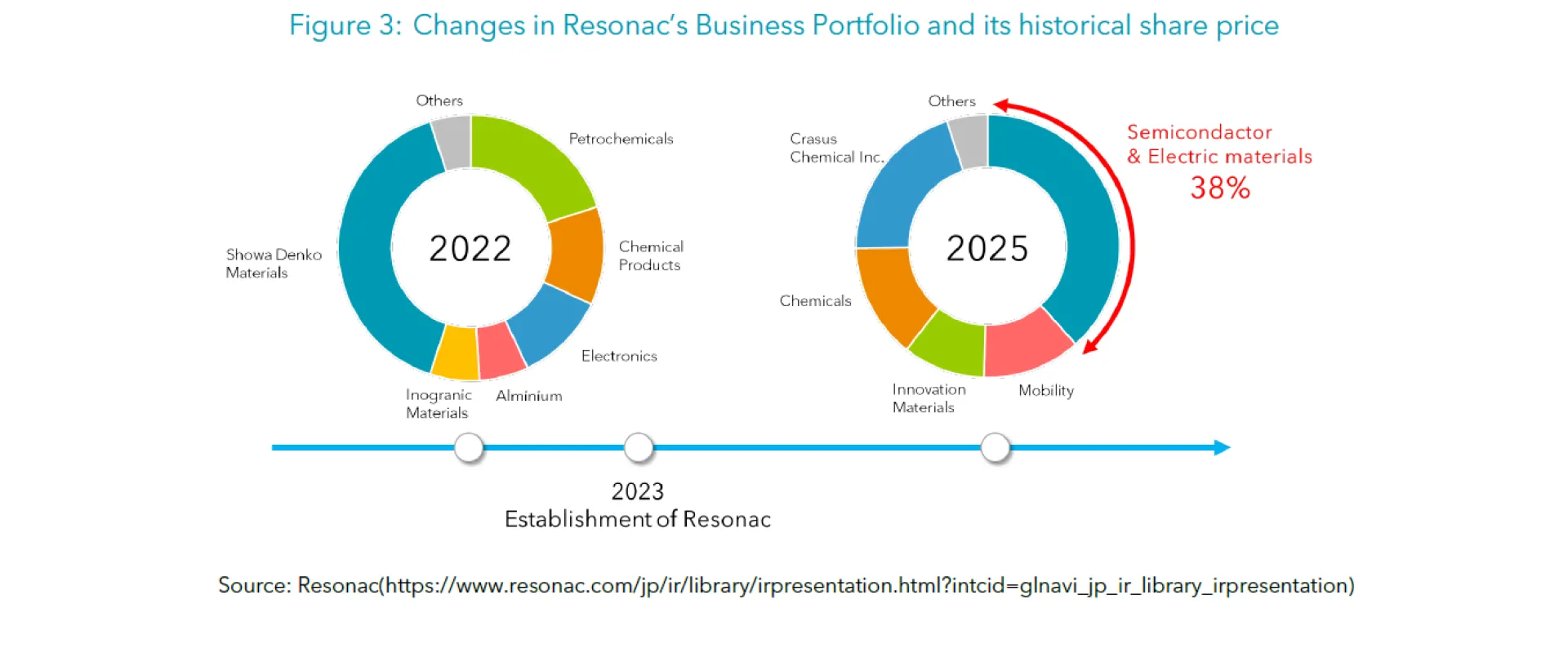

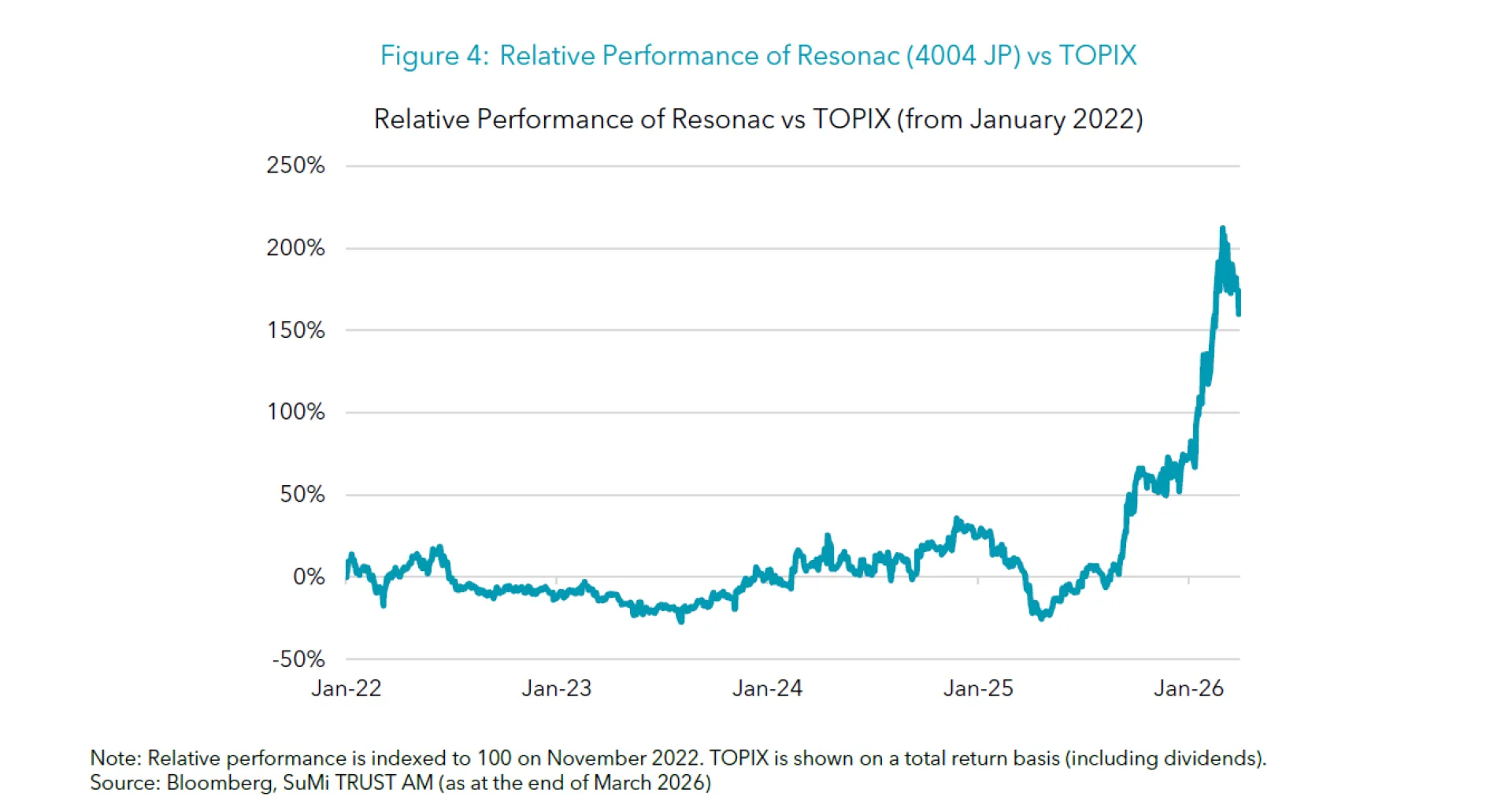

In the chemicals sector, we have identified companies implementing portfolio restructuring aimed at enhancing profitability over the longer term. For example, Resonac, a chemical company formerly called Showa Denko, has undergone a major transformation into a semiconductor-focused company, following its acquisition of Hitachi Chemical. The company has been retaining competitive businesses while divesting non-core operations. Whereas it was once regarded as a bulk chemicals producer susceptible to market cycles, it has been transformed into a highly specialised enterprise.

Such business portfolio reforms differ from purely financial measures; they are initiatives aimed at improving profitability and growth potential by strengthening the quality of the business itself. Structural measures to enhance corporate value influence not only ROE but also PBR through changes in the market’s expectations of future growth.

It is important to distinguish portfolio reforms like those undertaken by Resonac that enhance the company’s underlying earning capacity from short-term measures to boost ROE, such as share buybacks or balance sheet optimisation.

— Are all companies undergoing such changes? Moreover, share prices have risen significantly in recent years. Can we say that these reforms have borne fruit?

From a formal perspective, many companies have established governance frameworks, such as the appointment of outside directors. In practice, however, disparities remain. Even where outside directors have been appointed, there are cases in which individuals closely aligned with the president are selected, and in reality, they do not exert strong oversight of management.

In companies where little change has occurred, the mindset of top management often remains the primary constraint. Where founders or long-serving presidents wield significant influence and internal dissent is discouraged, superficial reforms alone are unlikely to bring about meaningful transformation.

That said, we have identified companies where outside directors are actively driving change, even in less high-profile cases where sell-side analyst coverage is relatively low. For instance, at textile firm Toyobo outside directors not only contribute at board meetings but also visit overseas operations to identify bottlenecks hindering improvements in ROE. Looking ahead, the distinction between nominal outside directors and those who genuinely contribute to enhancing corporate value is likely to become increasingly apparent.

Another notable development is the capital alliance between Berkshire Hathaway, Warren Buffett’s US investment firm, and Japanese insurance group, Tokyo Marine Holdings. Tokyo Marine has explicitly stated its aim of raising ROE to levels comparable with global peers, significantly above the 8% ROE common in Japan.

Taking these developments into account, I believe there remains considerable scope for further progress.

—From the perspective of a SuMi TRUST analyst, how do you distinguish between companies that have embraced corporate governance reform and those that have not?

SuMi TRUST’s research framework is characterised by strengths in organisational capability, staffing and access to management. We engage systematically with companies to promote value enhancement and, drawing on a substantial body of case studies of firms undertaking governance reform, we are able to identify those with a genuine appetite for transformation.

Companies that typically have a ‘willingness to change’ include those that are undervalued, those undergoing leadership changes (for example, a new CEO), and those where the number of dissenting votes at general meetings is rising.

In addition, with respect to engagement - including governance - our analysts work closely with the Stewardship Promotion Department. From a resourcing perspective, our equity analysts cover all sectors and monitor a wide range of companies. Supported by a substantial level of assets under management, we are also afforded frequent opportunities to engage directly with management as a major shareholder, which enables us to form forward-looking views on strategic direction.

By leveraging these strengths within our research framework and carefully identifying companies with a strong willingness to reform, we believe it is possible to significantly enhance the potential for generating excess returns.

3. Outlook and the Appeal of Japanese Equities

— In what direction do you expect future governance reforms to proceed?

The third revision of the Corporate Governance Code is scheduled for June 2026, indicating the new governance model remains a work in progress.

While it remains uncertain how the Corporate Governance Code itself will evolve, we believe the trend towards ‘management focused on share price and capital efficiency’, as promoted by the Tokyo Stock Exchange (TSE), will continue. Combined with increasingly stringent voting practices, companies will be compelled to sustain their efforts to improve both ROE and share prices.

We have also strengthened our own voting criteria for companies with low ROE. For example, we have raised the ROE standards to the top two thirds of the Topix constituents, from the top three-quarters previously. As a result, we vote against a significant proportion of company proposals - primarily on director appointments - exerting meaningful pressure on management. Coupled with the exclusion of persistently underperforming companies from the TOPIX and the overall improvement in market-wide ROE, the effective threshold has risen significantly.

— What is your view on the large cash holdings of Japanese companies?

Japanese companies hold substantial cash balances not only to fund future investment and working capital, but also due to a conservative approach to risk management. One possible explanation is a degree of distrust regarding banks’ lending behaviour, particularly the concern that lending conditions may tighten abruptly during periods of weaker performance. This, in our view, is one of the underlying reasons for their sizeable cash reserves.

However, simply accumulating cash does not enhance ROE. Going forward, there will be greater scrutiny of how capital is deployed -whether through investment, M&A activity, shareholder returns, or strengthening balance sheets.

Although the initial draft of the June revision to the Corporate Governance Code included explicit language calling for a reduction in ‘cash and deposits’, this was softened in the final version. While this is somewhat disappointing, the overall direction—namely, a greater focus on capital efficiency—is unlikely to change.

— Is there a risk that the current momentum in governance reform could reverse?

The likelihood of a return to the past is low. The shareholder base has already undergone significant change, and the era in which companies were shielded by stable shareholders has effectively come to an end.

That said, there is a possibility that the pace of reform may slow at some point—most likely when Japanese companies have made substantial progress in improving their performance. However, at present, there remains considerable room for further improvement. Achieving an ROE of 8% should not be viewed as the end goal.

In the banking sector, for instance, targeting ROE levels of around 12% over the coming years is increasingly becoming the norm. Similarly, more companies are following the approach of Tokyo Marine’s, which is aiming to achieve capital efficiency comparable with global peers in the insurance industry.

At the same time, long-term international investors are showing growing interest in these developments. While high-profile investments in Japanese companies are symbolically important, there is also a more fundamental shift underway, whereby improvements in capital efficiency and governance are driving a reassessment by global investors.

Japanese companies have already begun to change, but the reform process is still only partway complete. With the alignment of policy initiatives, engagement and voting by long-term investors, and the influence of activist shareholders, there remains significant potential for further enhancement of corporate value.

Ultimately, governance reform in Japan is transitioning from a phase of ‘formal and financial compliance’ - such as appointing outside directors or conducting share buybacks -to one of ‘substantive management reform’. Going forward, the focus will shift from simply improving ROE to examining the ‘substance of management’ itself: how capital is allocated and what kind of business structures are created. It is precisely in this area that we see the greatest investment appeal in Japanese equities.